Definitions

Construction Budget: The maximum amount of money, including contingency allowances, which the client is prepared to spend on the construction cost.

Construction Cost: The total cost of the work to the client to construct all elements of the project designed or specified by, or on behalf of, or as a result of coordination by, the architect, consisting of the construction contract price, cost of changes to the work during construction, construction management fees or other fees for the coordination and procurement of construction services, and all applicable taxes, except value-added taxes, which shall be excluded. Construction cost excludes the compensation of the architect and consultants, land cost, land development charges and other professional fees.

Construction Cost Estimate: The anticipated total construction cost at the anticipated time of construction, including contingency allowances, as determined or agreed to by the architect from time to time, the accuracy of which corresponds to the available level of detail of design development and the construction documents, and the extent of construction completed.

Construction Contingency: A reserve included in the construction cost estimate established to provide funds for the implementation of risk management strategies should risk events occur, including such events as the evolution of the design prior to construction, price escalation between the time of cost estimate preparation and construction, unknown conditions, and/or function and design changes made during construction.

Element: Term used in cost estimating to describe a component of a building, such as a sub-structure (footings, foundations) or envelope (walls and roof).

Indexing: Applying an index or factor to adjust costs from one geographic region to another (a typical index might be expressed as a percentage, such as 102.7%).

Program: Group of related projects and operations that are managed in a coordinated way to obtain the benefit that could not be achieved if managed separately.

Project: An endeavour undertaken within a defined period of time that produces a unique outcome.

Project Budget: The client’s estimated total expenditure for the entire project. It includes, but is not limited to, the construction budget, professional fees, costs of land, rights of way and all other costs to the client for the project.

Project Risk: The sum of uncertainties associated with a project undertaking.

Quantity Survey: A bill of quantities or a detailed listing and quantities of all items of material and equipment necessary to construct a project.

Introduction

The importance of construction project cost planning and control in the delivery of professional architectural services cannot be overemphasized. Clients are unlikely to allow their architect to proceed unless the architect first estimates the cost of a venture and then monitors the process. Cost management is more common today because of increased expectations for cost control, expertise in this field, and the availability of sophisticated analytical tools.

Providing Advice on Costs

In most client-architect agreements, one responsibility of the architect is to prepare an estimate of the probable construction cost. This estimate is neither a quotation nor a guarantee. Due to the variable market conditions, the architect should never guarantee or warrant a construction cost estimate. Such a warranty may void portions of an architect’s professional liability insurance policy. Nevertheless, the architect is expected to deliver the normal, professional standard of care in preparing an estimate of probable construction costs and providing cost advice.

Whenever suitably experienced personnel are not available in-house, architects or owners should hire the best available cost consultants. If preferred, the architect or cost consultant should form an alliance with business associates who are contractors or in the development industry, or they should establish an ongoing relationship with a quantity surveyor.

The Role of the Architect in Cost Planning and Control

Figure 1 Cost Planning and Control by Project Stage

To ensure that the project will be well-defined and realized within a predicted budget, cost management, including cost planning, cost analysis and cost control, requires:

- planning how costs will be managed and who is responsible for cost planning, control and monitoring;

- effective cost estimating;

- financial analysis of various components;

- management of the design and construction documentation process.

Cost planning, including the preparation of construction cost estimates, is done in the pre-design and design stages, whereas cost control or the monitoring of construction costs, is done in subsequent stages. See Figure 1.

Formats for the Presentation of Cost Information

The client usually summarizes overall program costs in a “global” or program budget which:

- lists all expenditures needed to complete every aspect of the venture;

- incorporates information provided by the architect for the design project and the construction project components of the budget with a detailed breakdown.

See Table 1 later in this chapter which illustrates “global” and “soft” costs that must be considered.

Prior to delivering cost advice on a regular basis, the architect should:

- make the provision of cost advice and project cost management a priority;

- make specific efforts to become knowledgeable;

- develop in-house experience and skills;

- maintain up-to-date records of historic cost data;

- emphasize to clients:

- the importance of cost estimating and related services;

- that a cost estimate is an estimate of cost, not a quote; and

- the need for a project contingency to provide for project risk, and that risk is inherent in any project endeavour.

To ensure effective cost management, every team member must be vigilant about the effect that all design, detailing or specification decisions could have on the cost of individual components of the project estimated during the initial budget preparation. The project manager will:

- initiate and control the preparation of cost information;

- manage team members to ensure that the work stays within the agreed-upon budget;

- set or adjust limits;

- exercise maximum influence on decisions affecting costs.

Once equipped with access to reliable and current cost information available at all stages of a project, architects should:

- use this resource with confidence;

- express information in standard formats;

- be consistent and methodical;

- avoid ambiguity;

- list all assumptions, constraints and limitations clearly whenever cost information is published;

- describe the factors considered in establishing the project contingency amount;

- promptly confirm in writing any cost information provided verbally;

- consider providing references and comparable projects when issuing information;

- start a cost information file for each project and keep it updated;

- analyze each project on completion (see Chapter 5.1 – Management of the Design Project);

- maintain files containing reliable historic cost data;

- check historic cost data in detail to ensure comparability with the current project.

Liability of the Architect

In an architectural practice, liability for incorrect cost estimates cannot be avoided, whether or not the architect is acting as the project manager or is providing limited services with no management responsibilities.

The typical client-architect agreement (such as RAIC Document Six – Canadian Standard Form of Contract for Architectural Services) will include a general condition that stipulates the terms under which an architect will be responsible for redesign at no cost to the client should the lowest tendered bid exceed the construction cost estimate by a predefined amount, often 10% to 15%.

Preparing Cost Estimates

Cost forecasting is an important and rigorous activity. All cost estimates:

- work on the principle of forecasting based on historic data;

- require that the original data be selected carefully and methodically by experienced personnel.

The success of any method depends on:

- the reliability of the raw historic data;

- the ability to adjust the data to suit the characteristics of the new project and to market conditions;

- the similarity of the new project in as many ways as possible to the examples from which data are available;

- the extent to which the analysis is broken down into a large number of small components, instead of a few large unit headings;

- how the project uncertainty and risk are provided for, with the inclusion of cash allowances and a contingency reserve.

Therefore, historic data must contain as much descriptive detail as possible, so that differences may be identified, and precise adjustments made.

Format of Cost Estimates

There are two widely accepted formats in which construction cost information is presented: Uniformat II and MasterFormat 2016, both developed by Construction Specifications Canada and the Construction Specifications Institute. These two formats relate through cross-referencing tables.

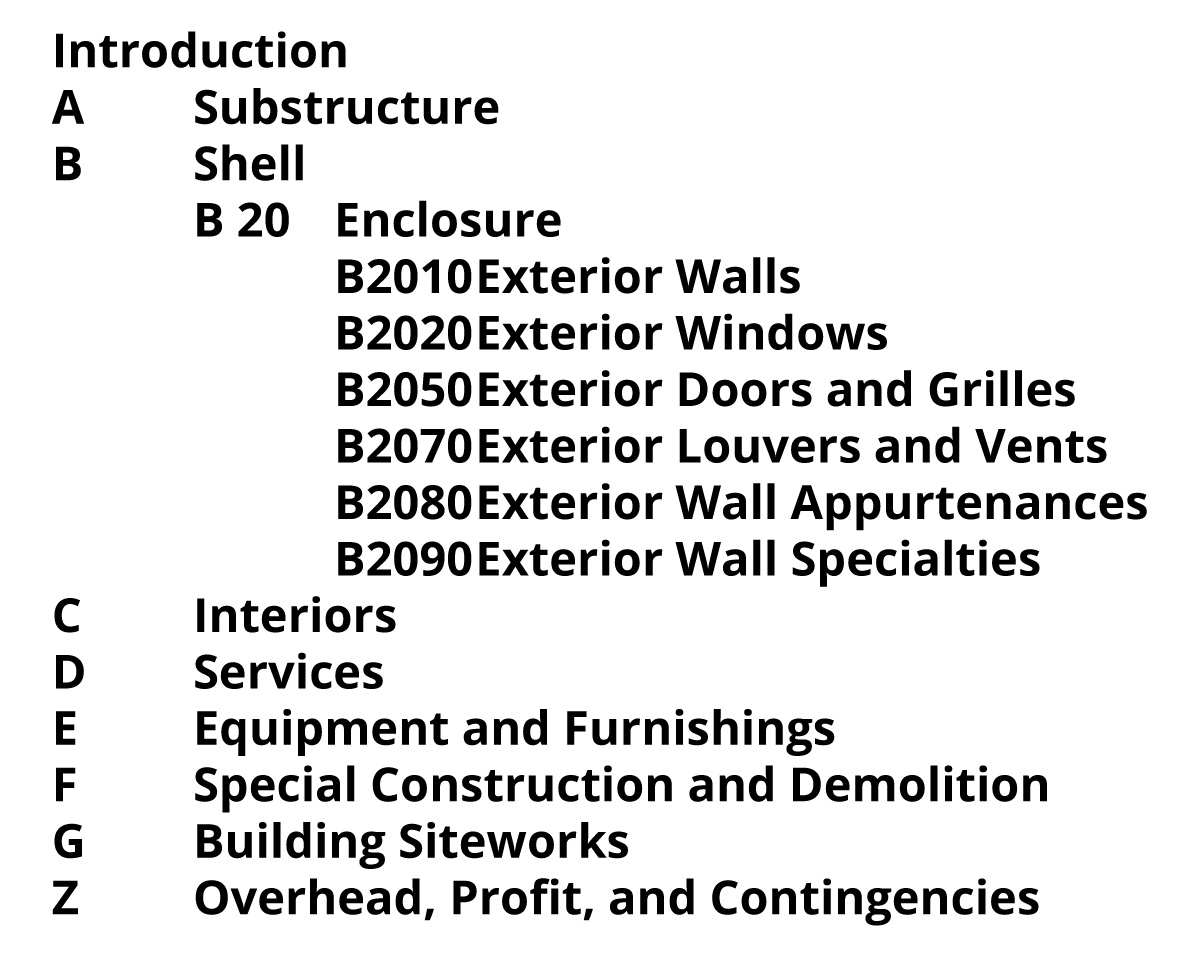

Uniformat, and then Uniformat II, were developed for the purpose of cost estimation. Uniformat is a structured system of eight major categories, A through G and Z. Each category is divided into major systems, then subsystems, then components in a cascading numbering system.

The breakdown allows for consistent presentation of cost estimation information through successively more detailed cost estimates.

The standard MasterFormat 2017 48-division system uses the trade and supplier headings that will eventually be used during construction. This same format is usually used by contractors for preparing tenders and for the preparation of applications for payment. The data in this format simplify retrieval (from files or electronic sources) for calculating detailed budgets for the next project. In preparing a bid, the contractor will divide the construction documents into trade groupings based on the MasterFormat categories. Each trade will provide a bid for their part of the work. The contractor then sums the bid groupings into a single bid.

Methods of Cost Estimation

There are several methods for estimating construction costs:

- analogous (or top-down);

- parametric;

- bottom-up.

Analogous Cost Estimating

An analogous cost estimate is performed when little, if any, information is available about the project at hand. It is very inexpensive and quick but its accuracy is highly questionable. However, it is what many clients desire prior to engaging an architect or expending any funds. For example, an architect may be asked about the construction cost for a new office building but has no information on the size or quality of the building. The architect may reply, “Well, I completed a four-storey office building last year for $7.5 million.” An analogy is drawn from a previous project when no information is available for the current project. It is an unfortunate reality that a construction cost estimate given in haste, sometimes under pressure, will become the benchmark for the rest of the project. The architect should reinforce that an analogous estimate is worth about the same as the paper it is written on.

Parametric Cost Estimating

The most common method used for estimating construction cost during design is a “parametric” estimating. Parametric estimating applies a measurement of a building, system, or component against a known cost per unit. For example:

- size of the building in metres X $/sq. m.;

- area of flooring X $/sq. m.;

- length of steel lintels X $/m.;

- number of light fixtures X $/supply and install of fixture.

A parametric estimate may be based on any form of measurable quantity, provided there is historic data that can ascribe a cost to the unit of that measurement.

Parametric estimating requires that the design team has developed the design to the extent that a cost estimator can reliably perform a take-off of measurable functions, areas, volumes, systems and/or components. A parametric estimate based only on a building’s square area could be performed quickly and economically; however, it may not result in an estimate with accuracy beyond an order of magnitude. A detailed parametric estimate based on systems and components will take much longer and cost considerably more, but will provide an estimate of a correspondingly greater accuracy.

Bottom-up Cost Estimating

When preparing a bid for a construction project, the general contractor and trades will perform a “bottom-up” estimate. It is referred to as bottom-up because the work is analyzed from the bottom of the project’s work breakdown structure and aggregated up to the subdeliverables and deliverables. The bottom-up estimate is the result of analyzing the work in detail, including estimates of the effort hours, labour rates, materials, logistics and overhead. The bottom-up estimate is the most accurate but requires extensive effort from all parties in the construction endeavour.

Applying Cost Estimating Methods

Elemental Costs Using Uniformat II

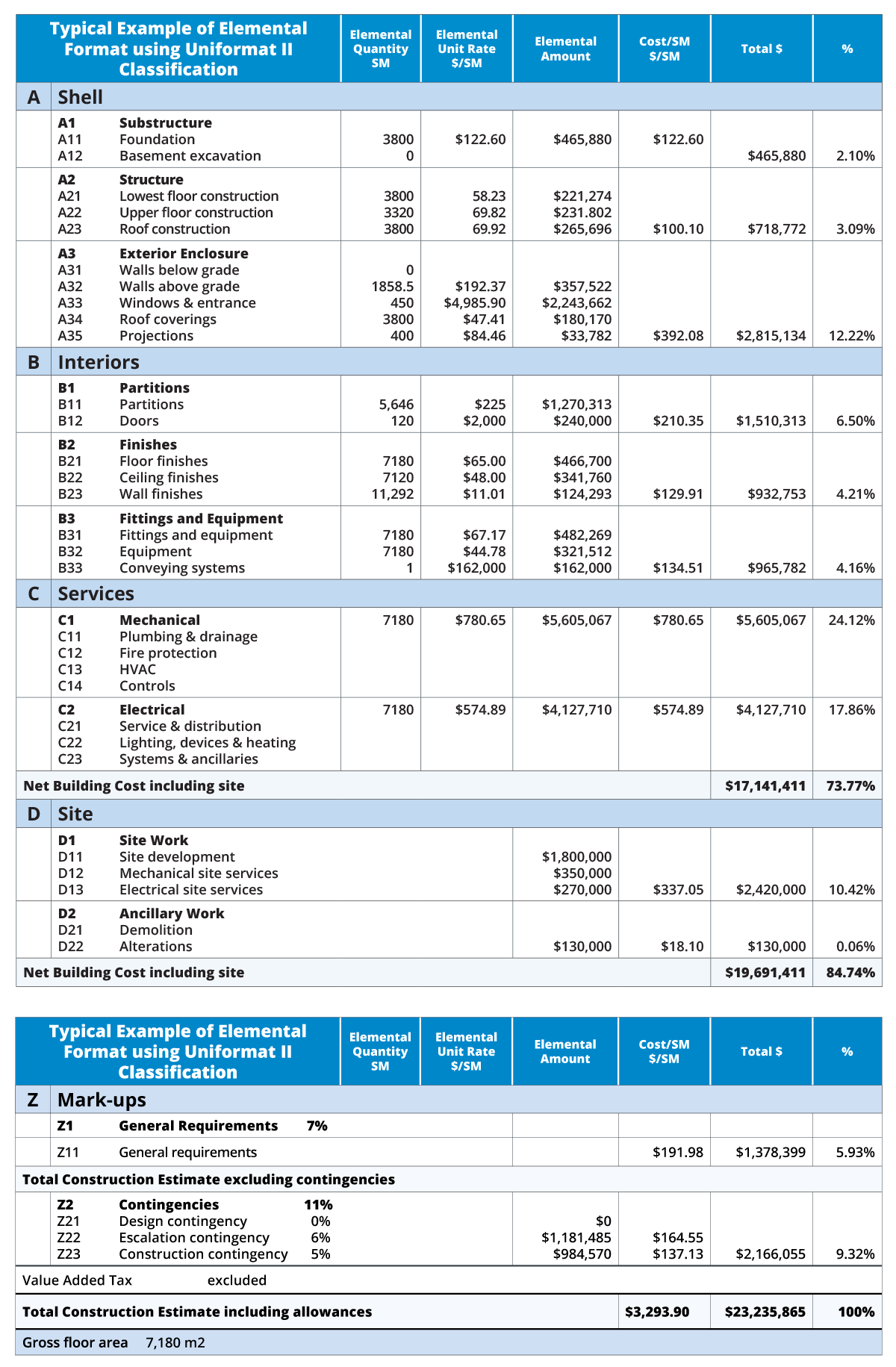

Elemental costing is more a presentation of cost information rather than a method. Parametric estimating is applied to the design and the amounts are aggregated into Uniformat II categories. Quantity surveyors often use the elemental cost method as the standard format for presenting cost information. This method:

- divides the building into systems and subsystems, such as structure and exterior closure;

- uses these elements to provide a cost framework which is useful throughout the life cycle of the project;

- is applicable to new or existing buildings;

- uses these elements to form the basis for applying relevant cost information from similar projects.

Advantages:

- the process assumes that the approximate size of a building is known;

- the process can proceed without construction drawings and specifications;

- particularly useful for architects during design development, when trade-offs between elements can be considered to improve the quality of the project without compromising the total budget.

Disadvantages:

- cuts across the traditional construction trade areas (see the “Classes of Cost Estimates” section above), therefore can be difficult to compare estimated cost information to actual cost information due to the different systems, i.e., Uniformat II vs. MasterFormat.

The elemental cost method is used by quantity surveyors or those experienced in the calculation of building costs.

See Table 4 for a typical elemental cost forecast.

TABLE 1 Typical Example of Elemental Format using Uniformat II Classification: Elementary School, 2 storeys, 21 classrooms

Parametric Estimating: Area

(Cost per m2/Cost per ft2)

The terms “cost per square metre/per square foot” are used throughout the development and construction industries, and are recognized by public and private institutions and the public at large. Both imperial and metric measurements continue to be used.

Extensive floor area cost data are available from a number of sources as a basis for interpolation and use in forecasting. These should be used when providing general cost advice and for the calculation of overall project costs.

Advantages:

- the concept of “floor area” is easily understood and applicable to all buildings;

- costs for an individual component or element of a building, or for the entire structure, are straightforward to calculate;

- very simplified historic cost information, expressed as costs per m2/per ft2 for completed projects, is available for many different building types.

Disadvantages:

- does not account for unique conditions or special construction;

- is simplistic and can be misinterpreted.

The architect should limit the use of this basic information by using it only as a general guide at the pre-design stage.

Parametric Estimating: Volume

(Cost per m3)

This method is not widely used, except:

- for certain specialized building types such as warehousing (particularly freezer buildings);

- for multi-storey buildings where the floor area method might not adequately reflect the true costs;

- as a double-check on the other methods being used.

An example of a parametric estimate based on volume may be found in Rough/Advanced Guide to Construction Costs, Section 2.1, published by the Toronto Regional Real Estate Board.

Parametric Estimating: Unit Use

(Cost per bed, cost per seat, etc.)

This method uses simplified historic data as a basis for calculating cost. It is brief, to the point, and relatively reliable – provided that the historic data on projects are comparable. This method is useful for preliminary budgeting because the result is general in nature and more obviously “approximate.”

Advantages:

- provides a quick reference or check at the early design stages.

Disadvantages:

- projects are rarely identical, so careful adjustment must be made for differences;

- the circumstances, location and date of construction may render the historic information of questionable value, even though the projects may be very similar in physical form;

- the calculation of differences may require extensive analysis of the information using some of the other methods referred to above (sometimes, this is best done by quantity surveyors).

Architects should:

- use this method with caution, for preliminary advice only, and as a convenient double-check for comparison purposes;

- spell out clearly all qualifications and assumptions when the information is released.

Do not confuse unit use with the term unit cost which can be expressed in several different numerical unit forms and is a technique used for calculating building and component costs:

TABLE 2 Unit Cost vs. Unit Use Cost Estimation (Note: Figures used as approximations and not to be assumed to be accurate.)

Classes of Cost Estimates

Government and institutional clients commonly use a classification method to align the projected accuracy of a cost estimate with the project phase. The classification of estimates, ranging from least to greatest accuracy, are titled Class D through Class A. Refer to “Appendix A – Description of the Classes of Estimates Used by PSPC for Construction Costing of Building Projects” at the end of this chapter.

The following are general descriptions of each class level:

- cost estimate Class D:

- performed at functional program phase, based on:

- information and historic data;

- adjustments taking into account assumptions regarding inflation, location, risk, quality, size and project timing;

- prepared prior to commencement of the design;

- a rough order of magnitude;

- estimating range of between ±20% and ±30% (Canadian Construction Association, 2012).

- performed at functional program phase, based on:

- cost estimate Class C:

- performed at schematic design phase;

- prepared at an early stage in the project, when drawings are preliminary in nature, based on:

- type of construction and quantities of materials;

- all assumptions or qualifications to the estimate;

- a relatively large design contingency allowance, which is used to provide for changes in scope and because information is more limited;

- estimating range of between ±15% and ±20% (Canadian Construction Association, 2012).

- cost estimate Class B:

- performed at design development phase;

- the estimating process is repeated when additional specification and drawing information becomes available, using an expanded format under the original headings;

- the reduction in uncertainty made possible by better information from the design team allows for a reduced design contingency allowance;

- estimating range of between ±10% and ±15% (Canadian Construction Association, 2012).

- performed at design development phase;

- cost estimate Class A:

- performed near or at completion of the construction document phase;

- as the construction documents become more complete, the process continues, and the contingency allowance is reduced further;

- estimating range of between ±5% and ±10% (Canadian Construction Association, 2012).

- performed near or at completion of the construction document phase;

Advantages:

- the most reliable method if undertaken carefully from the start;

- well-suited when cost advice is being supplied to the architect by contractor/construction managers and suppliers;

- the information stays current and relevant throughout pre-construction;

- project leaders can build up a history of, and the knowledge and skills for, cost estimating – especially if building projects are similar within the architectural practice.

Disadvantages:

- requires an estimator with both design and construction experience;

- requires the ability to foresee all the typical trades needed to complete the building.

Sample Cost Estimate Breakdown Over the Design Project Life Cycle

Tables 3, 4 and 5 following feature a sample build-up, from summary to detail, of a cost estimate for a typical industrial manufacturing building over the design project life cycle. Table 3 illustrates the total project summary. Table 4 illustrates the summary construction budget in MasterFormat® (2017 48 division format). Table 5 provides the detailed breakdown of Division 03 – Concrete.

(Click below tables for PDF versions)

TABLE 3 Sample Project Cost Estimate for a Typical Industrial Manufacturing Building

Table 4 Sample MasterFormat Cost Estimate Summary Page

TABLE 5 Sample Detailed Information - Division 03 - Concrete

Factors Affecting Costs

Economic and Political

Several factors influence the construction industry and affect building costs. These factors include:

- inflation;

- market conditions;

- other economic factors;

- political and social climate.

Inflation

Due to economic cycles, inflation and the consequent escalation of construction costs can vary, depending on the era and the economic factors affecting Canada and the world. Because inflation is a factor of the cyclical economic system, especially for construction, architects should:

- always include an allowance for escalation as a line item in the project budget;

- be aware of the trend during the past 12 months as well as predictions for the future;

- indicate a reference date on all estimates;

- seek input from the client.

Market Conditions

Periodically, there is so much demand for construction that it can become almost impossible to obtain competitive tenders for a project. This situation results in inflated costs. At the other extreme, construction costs during recessions – particularly for non-union labour rates – may decrease significantly. Such decreases can be followed by a rapid rise in costs shortly after the end of the recession.

Other Economic Factors

- the use of union or non-union labour;

- interest rates on financing costs;

- large demand for certain building materials;

- exchange rates between nations, for projects with a significant proportion of imported materials and equipment.

Political and Social Climate

In Canada, the political climate (local, provincial and federal) can affect the timing of a project approval, especially around election time.

Abroad, in countries where democracy and respected institutions are stable, commercial activity can flourish, and competition and true supply and demand will occur. In certain areas of the world – where some or all of these factors may be missing – stability is often lacking, and construction prices will tend to be erratic and unpredictable.

Prior to using any raw cost data for estimates, architects and cost consultants should consider all the above factors and make suitable corrections.

Site Context and Climate

Construction costs are affected by several environmental factors:

- site characteristics;

- weather, and season of the year;

- location.

Site Characteristics

- challenging topography;

- natural or built features;

- unusual soil or sub-surface conditions;

- existence of hazardous wastes, including asbestos and PCBs;

- contaminated soils requiring removal and/or environmental certification;

- disposal costs of contaminated soils;

- adjacent buildings.

Weather and Season

- cost and construction procedures in Canada are significantly influenced by the weather and season;

- construction activities are cyclical over each 12-month period (reduced activity from December through March for exterior construction and excavation);

- winter protection and provision of temporary heating adds to cost.

Location

- site characteristics (for example, a project in a suburban location will cost less compared to one in a constricted downtown core – where overhead can be much higher because of parking charges, traffic congestion causing loss of time and delivery delays, and the likelihood of more stringent regulatory requirements);

- construction in remote areas where skilled labour is unavailable;

- distance to sources of supply for materials and trades;

- use of components that are manufactured at some distance from the site;

- travel distance to dump/disposal sites or recycling depots

Building Type and Design

Building types range from simple wood-framed structures to complex, technically sophisticated buildings such as hospitals and laboratories. Some costing handbooks classify building costs under several dozen different types. Construction costs vary considerably, from a warehouse building, $896.97 $/m2, to a performing arts centre, $4,719.33 $/m2 (Canadian dollars 2018).

Features affecting cost include:

- compliance with building codes;

- method of construction (for example, wood, reinforced concrete or steel frame);

- building height and number of storeys;

- building form (a compact building is less expensive than one with the same area that is long and narrow);

- type and range of finishes;

- choice and arrangement of structural, mechanical and electrical systems;

- the planned life of the structure;

- selection of components (standard or off-the-shelf vs. custom-manufactured);

- sustainable design requirements such as material selection and requirements for certification.

Characteristics of the Owner/Client/Stakeholders

Architects need to recognize the impact that the type of owner can have on the cost of a project.

Sophisticated clients, such as commercial and industrial corporations or developers who regularly procure design services and construction, frequently expect the delivery of completed projects at or below target costs.

Government agencies and public institutions are increasingly eager to find avenues for value generation and cost savings, but may be restricted from certain procurement methods due to regulations and key stakeholder interest and influence. These may restrict the organization from approaches common among private sector client groups. Many factors contribute to project costs, and the role of both the client and the design team is to influence those factors, where possible.

Process and stakeholder requirement factors that affect construction project costs include:

- design requiring high standards of quality;

- rigorous quality control procedures (especially long life cycle, redundancies in spaces);

- limited authority or control over key stakeholder by the owner’s representative;

- complex bidding procedures;

- insurance requirements above the norm;

- bonding requirements beyond industry norms;

- poorly written, sometimes inequitable, non-standard contract wording;

- long delays in issuing payments to contractors.

The architect should act proactively to consider construction cost estimate adjustment factors that reflect the client’s organizational priorities, culture, context and stakeholder relationships.

Definition of Project Requirements (Functional Program)

See Chapter 6.1 – Pre-design.

The functional program defines the owner’s and users’ functional requirements for the design project. To minimize the possibility of cost overruns resulting from changes in the program, review the functional intent or objectives.

The architect should act proactively to mitigate two project risks frequently experienced: requirements of unidentified stakeholders and unstated stakeholder requirements. The functional programming development exercise may not have addressed the needs of all stakeholders, or certain stakeholders may have been denied the opportunity to provide input. The practical reality of this situation is that stakeholders who have been denied input may exert political pressure within their organization to have their requirements included within the project scope. The impact on the architect may be that the architect is expected to make design adjustments without additional fees or extending the schedule.

Apparent cost overruns may be the result of a functional program that was not validated against the construction cost estimate. A functional program may not have received detailed and critical analysis prior to being received by the architect. The architect should discuss with the owner how the functional program was created and validate that the information contained in the program is current, accurate and complete. Ask the owner to clarify any incomplete or unclear requirements prior to providing any architectural service.

Changes in the scope of a project can occur for many reasons, including:

- the development of more specific, detailed requirements by the owner;

- external factors such as new technological developments, new legislation or a change in market conditions;

- lack of sufficient detailed information;

- a change in client personnel, building users or stakeholders;

- inadequate research prior to developing the program;

- the addition of new partners or stakeholders.

Cost increases due to changes in the program can be significant for the owner and the architect at any time, but especially in the construction documentation stage, when re-design costs and additional consulting fees arise.

The architect should always keep the owner fully advised of the potential cost implications of any changes.

Type of Construction Project Delivery

Contractual relationships between the owner and the contractor can have an impact on the cost of a project. See Chapter 4.1 – Types of Design-Construction Program Delivery.

Owner’s Responsibilities and Timetable

Owner requirements beyond industry-accepted practices or norms can affect the construction budget. In all cases, these requirements should be discussed with the owner. Some of these circumstances include:

- a project schedule that is accelerated to suit an owner’s critical date, such as a school opening or the timing of an event due to market forces;

- construction work conducted only during hours when the building is not otherwise occupied, e.g., evenings and weekends;

- late commencement due to reasons beyond the owner’s control, for example, winter conditions, resulting in additional construction costs;

- delayed commencement of a project during a time of inflation and currency fluctuations;

- owner’s approval processes.

Architects are advised to:

- ensure that assumptions attached to any forecasts include reference to specific timing;

- check and make adjustments for specific issues that may influence the cost of the project when using historic cost data.

Ultimately, the owner’s requirements are what they are, and the design and construction teams need to proactively address the owner’s needs.

Other Factors

Regulations:

- regulatory and by-law requirements, such as planning approvals or site development agreement conditions;

- numerous building code occupancy classifications within one building;

- hazardous demolition, such as remediation of designated substances (asbestos, lead, etc.);

- recycling regulations and dumping charges (tipping fees) for demolition or construction debris.

Inconvenient or unusual work arrangements:

- construction that must be scheduled around the ongoing activities of occupants in buildings such as hospitals, court houses, education facilities, shopping malls, or restaurants, resulting in a departure from normal construction work or scheduling and overtime labour costs;

- additional protection and clean-up expenditures beyond normal requirements;

- work adjacent to or within certain building types that may be subject to limitations on scheduling and on the times when equipment, such as cranes, may be used;

- demolition and shoring of existing structures;

- extensive construction phasing.

When developing the cost plan of a project, establish the basic cost of the building. Identify and pull out unusual or site-specific costs and justify the overall project budget during the forecasting process.

Techniques

Cost Consultants

Unless the architect has developed the knowledge and systems in-house, expert advice should be obtained from:

- independent professional experts (quantity surveyors); or

- those intimately involved in everyday construction (development/construction experts).

Quantity Surveyors

Quantity surveyors provide professional services at hourly rates, or at a fixed fee or percentage fee of the construction budget.

Advantages:

- independent professional status;

- their success is based upon their track record of reliability in forecasting;

- up-to-date archival material that is very extensive for many different building projects and is easily accessible;

- quantity surveyors will usually supply information on comparable projects as a double-check to establish credibility;

- some larger companies publish their own updated forecast information yearly.

Disadvantages:

- unit costs are usually historical and often not connected to real-time costs, making them less current than costs available from contractors or construction managers;

- detailed cost information may not be available because cost breakdowns are limited to major trade divisions.

Cost estimating is as much an art as a science, and architects are advised to:

- use the services of a quantity surveyor whenever appropriate, to increase the quality and depth of the architectural service available within the practice;

- monitor every aspect of their work to ensure that the information being prepared is entirely applicable to the current project, and that any qualifications or assumptions accompanying the cost information supplied are precisely in accordance with the client’s expectations;

- be satisfied that every item of information is relevant before passing on this advice to the client;

- ensure there are sufficient fees:

- for coordination when a construction manager is involved, or when value analysis or value engineering is undertaken;

- to include the quantity surveyor’s fees or cost estimating.

(Note: Some clients prefer to engage a quantity surveyor directly; in these situations, the architect should allow for fees for coordination.)

Construction Managers and Other Development/Construction Experts

Other sources of expertise directly from the construction industry include construction managers, contractors, design-builders and developers.

Advantages:

- reliability of cost calculations for various classes of cost estimates increases using unit costs assigned to area measurements for spot-checking individual elements of a project where the proposed building is very similar to recently completed projects;

- information will be very current because these sources are involved with construction spending every day, and because they have access to trades and suppliers who are also specialists;

- these sources monitor trends and are generally aware of the dynamics affecting construction costs.

Disadvantages:

- unlike a quantity surveyor, who is an independent consultant, the builder may not always present a comprehensive overview of all costs;

- this knowledge is sometimes very specialized and “narrow,” and may not always be applicable to new situations;

- certain sources may be less reliable due to possible self-interest or commercial motives;

- architects should consider:

- developing an alliance with individuals or companies by working together on common projects before using this source for cost information;

- checking the relevance of all data supplied, even if they have confidence in the information source;

- paying a fee for all cost information from construction industry sources.

It should be noted that when there may be a conflict of interest, information from a “free” source may not be reliable.

Construction Price Index

Construction price index data are usually published by government agencies and private companies. These publications are:

- useful only as a guide to show trends;

- usually some months out of date;

- often presented in graph form for ease of communication.

Publications

Construction cost data are available from government agencies, private interest groups, private companies and quantity surveyors. The information comes in printed or electronic form, and the cost varies considerably depending on the amount of detail, completeness and ease of use. Data from government agencies are more useful for identifying trends and differences in national, regional and local costs than for calculating the cost of a specific building.

Extensive detailed information for most building types can be purchased in hard copy or electronic form. Such publications:

- provide excellent, comprehensive and reliable data if used with appropriate qualifications or multipliers;

- are assembled from real project data supplied by owners and contractors from the previous year;

- are available for Canada only, or for all of North America (amounts can be adjusted to the individual cities or regions).

The data may be used for entire buildings or individual components. Note that the data are more reliable for estimating in Canada when obtained from Canadian publications or sources. Data from non-Canadian sources may not be reliable for estimating purposes when the value of the dollar is fluctuating.

Architects should:

- build forecasts using these data carefully and methodically;

- carefully read the descriptions of the scope and cost allowances to ensure that the proposed building estimate is based on a comprehensive list of items which apply exactly;

- become familiar with the formats and methods employed prior to using any information.

Contingencies

Every budget estimate should present a prediction of the final cost of the completed project. In practice, this means that contingency allowances of decreasing size must be applied to project and construction budgets as relevant information develops during the design process.

There are two contingencies and it is important to distinguish between design contingencies and construction contingencies, and identify both in any estimate in addition to any escalation amount. Contingencies, which may be as high as 25% at the early stages of a project, will decrease to 2%–5% as the degree of uncertainty is reduced. Construction contingencies for renovation work are higher.

Most government agencies involved in construction, as well as private companies, banks and other financial institutions, expect a single contingency amount to be shown at the bottom of a budget. This figure, giving the full extent of the contingency allowance, can be plainly seen. However, some project managers prefer the contingency to be apportioned for each line item, in addition to showing a general contingency at the end.

Professional Service for Each Phase of the Project

Use a checklist such as the “Checklist for the Management of the Architectural Project” (at the end of Chapter 5.1 – Management of the Design Project) to ensure that all cost estimating tasks are attended to at the appropriate time.

The sections below are a commentary on the lists of tasks.

Phase A. Pre-agreement Phase

By listing all cost-related tasks, the architect:

- ensures that every aspect of spending on the project will be reviewed by either the architect, the client or another party;

- can prepare a complete proposal for services.

The purpose is to:

- make the client aware that this service will be required to complete the entire project;

- identify who will be responsible for investigating and supplying the forecasting information.

Phase B. Schematic Design Phase

In this phase, the architect establishes a preliminary design and a construction cost estimate for the project, based on the most reliable information available at the time from consultants and other specialists. The architect may either:

- instruct the design team to continue with conceptual work that will meet or satisfy the agreed-upon budget; or

- review the scope, quality and cost for some or all of the building elements to re-define the project to fit within a pre-determined cost limit; or

- revise the budget and re-define the scope of the project.

Using up-to-date cost forecasting information, as well as carefully defining the project scope and cost limits for the project elements, will minimize the risk of significant re-design and re-definition later.

Phase C. Design Development Phase

In this phase, the architect may:

- provide for review and updating of the construction cost estimate as the reliability of the design and specifications improves;

- undertake additional analysis, if necessary, to check the construction cost estimate and its assumptions;

- refine the building’s scope, design, quality and details to ensure they will not exceed the limits of the construction cost budget.

Phase D. Construction Documentation Phase

In this phase, the architect may:

- update the construction cost estimate based on the construction documents (often at 50% completion and at 95% completion – the pre-tender stage, or at other defined milestones);

- include allowances in the bid documents.

See Chapter 6.4 – Construction Documents: Drawings and Specifications.

Phase E. Bidding and Negotiation Phase

In preparing the bidding documents, the architect must determine what cost information is needed. The architect must consider the following cost information:

- alternative prices;

- itemized prices;

- unit prices;

- cash allowances;

- addenda.

Refer also to CCDC 23 – A Guide to Calling Bids and Awarding Construction Contracts.

The architect’s role is to analyze the bids received from contractors. The various “alternative prices” from each bidder must be evaluated and the best overall value for the client determined. The lowest combination of base bid and acceptable alternative prices may be the choice of greatest value to the owner, but both owner and architect must be mindful of bidding law and ensure that the bidding process is not tainted through preferential treatment of one bidder over others.

Itemized prices are costs for a specific item or section of work for information purposes only. Unit prices should only be requested when an estimated quantity is difficult to provide or there is an anticipation that additional material beyond those stated on the contract documents will be required. Unit prices are typically requested for large civil engineering projects; however, certain components (such as site development work, hidden or indeterminate work) within architectural projects may require unit prices.

See also Chapter 6.5 – Construction Procurement.

Canadian Standard Form of Contract for Architectural Services indicates that if the lowest bona fide bid exceeds the construction cost estimate by a predetermined amount identified in the agreement, the architect shall either:

- obtain approval from the client for an increase in the construction budget;

- re-bid or negotiate; or

- modify the construction documents to reduce the construction cost (for no additional fee).

Phase F. Contract Administration Phase

The architect is usually required to determine the amounts owing to the contractor under the contract, based on the architect’s observations and evaluation of the progress of the work. The architect then processes the contractor’s application for payment and prepares a certificate for payment. The elemental cost analysis method is well-suited for use on a comparative basis in assessing the contractor’s schedule of values submitted at the outset of the construction phase. Another architectural service provided during the contract administration phase is the evaluation of the costs of changes. Having ready access to historic cost data, to ensure that the contractor’s quotations are realistic, is very important.

See also Chapter 6.6 – Contract Administration – Office and Site Functions.

The architect usually:

- delivers effective cost management service throughout the project;

- provides the owner with regular cost updates and advice (this will occur naturally to some extent during the construction phases when the client receives copies of proposed changes, change orders, and certificates for payment);

- endeavours to maintain the supply of excellent cost advice and well-presented information throughout a project.

Life Cycle Costs

In the past, building costs often considered only initial or capital construction costs and did not always include costs associated with operations and maintenance. Recently, high energy and maintenance costs have highlighted the fact that the “real cost” of a building is not limited to the construction phase. An analysis of life cycle costs is not a basic service but an optional or additional service.

The objective of life cycle costing is to determine the “total cost” of a building over its lifetime. This costing method:

- allows comparisons to be made between alternative components or systems;

- generates an understanding of the design of a project, how it functions and how costs arise;

- facilitates further development of the design.

Life cycle costing of a building can be expressed as follows:

Total Cost = Capital Cost + Operating Cost + Maintenance Cost

The three types of costs are:

- capital costs: the initial cost of constructing the project, including the land, fees, and carrying costs;

- operating costs: all expenditures for the servicing of the building during its life period, for example, lighting, energy, management and insurance;

- maintenance costs: those costs associated with repairs and renewals.

The total cost as defined above is relevant to the long-term costs of owning a building and is of special interest to owner-occupiers such as government bodies, condominium corporations and large institutions.

Before the design development phase begins, the architect should discuss the importance of life cycle costs with the client for the following reasons:

- different construction materials, techniques and systems have different effective life spans;

- considerable expense can arise during the life of a building to maintain a satisfactory level of performance;

- low construction costs may result in higher maintenance costs later in the life of the building.

Using a pre-determined and agreed-upon “design length of life” as a base, the life cycle costs analysis will:

- assess the initial, maintenance, and replacement costs for each element of a building (for example, different types of mechanical systems and roof membranes can vary significantly in initial cost and in their anticipated serviceable life);

- compare this information with total costs for alternative selections or designs;

- study different combinations of all major elements to identify the best choices to minimize capital cost;

- determine the most advantageous or lowest life cycle cost for the entire structure;

- incorporate operating costs, including energy consumption, in the study.

Architects can effectively undertake most life cycle cost comparison exercises if they have access to adequate cost and material specification information. A more detailed analysis should be undertaken by qualified specialist consultants.

Value Analysis or Value Engineering

Sometimes a project will be subjected to value analysis or value engineering. This service is not a basic service of the architect and is frequently undertaken with the use of an external facilitator. The best time to apply any value analysis is early in the design process. One limitation of value engineering is that it generally does not take into account the architect’s logical and sometimes intuitive design process.

Value engineering is a systematic procedure to determine the best or optimum value for investments in a construction project. The terms “value analysis” or “value engineering” should not be understood as pseudonyms for cost-cutting.

During value analysis architects usually work with cost consultants and value engineers to compare trade-offs between design concepts, arrangements, materials and finishes, systems and construction techniques, as well as capital and life cycle costs. This analysis should begin during the schematic design phase when conceptual drawings and outline specifications are prepared. Ideally, value engineering is planned and scheduled at the outset of a project; however, the architect should be willing to undertake such a study at any stage of the project. As noted above, the best time for value engineering is early in the design process.

Certain project delivery methods are better suited to value engineering, and different owners will apply different criteria for such studies. For example, developers or design-builders may plan to dispose of an asset soon after construction, with more interest in reducing capital spending and less interest in life cycle costs. Landlords and building owners may be more concerned about reduced operating and maintenance costs as well as lower replacement costs. Lower capital costs are almost always a significant consideration. The objective should be to minimize construction cost while maintaining quality through the substitution of alternative materials and systems.

The owner may choose to engage an independent reviewer, rather than the architect/engineers of record, in the belief that this will be more likely to achieve the desired results. This approach can sometimes result in the substitution of inferior or inappropriate products, simply because they are cheaper; this is not true value engineering but rather cost-cutting. In these circumstances, the architect must be informed and given the opportunity to advise the owner on the consequences of the proposed changes.

The architect should document all changes in construction documentation requested by the owner. The architect should provide written comments and recommendations on all changes, and clearly describe the positive and negative aspects of the substitutions.

Embodied Energy Cost Analysis or Embodied Energy Consumption

This type of cost analysis assesses the environmental impacts and energy consumption resulting from the extraction, manufacture, delivery, installation, demolition, and recycling of building materials in buildings.

Increasing emphasis is being placed on the need to conserve natural and manufactured building materials and to reduce the embodied energy contained within all products used in building construction.

Work in this field is frequently undertaken by specialists. Architects are well equipped to develop knowledge and skills in this area of expertise, rather than relinquishing the field to others.

References

Canadian Construction Association. “Guide to Cost Predictability in Construction: An Analysis of Issues Affecting the Accuracy of Construction Cost Estimates.” 2012. https://www.cca-acc.com/wp-content/uploads/2016/07/GuideCostPredictability.pdf, accessed April 24, 2020.

Canadian Institute of Quantity Surveyors. “Quantity Surveying and Cost Consulting Services: Schedule of Services and Recommended Charges, Sixth Edition.” 2012. http://www.ciqs.org/english/available-services, accessed September 14, 2020.

Canadian Institute of Quantity Surveyors. “Method of Measurement of Construction Works, Eighth Edition.” http://www.ciqs.org/publications/method-of-measurement-of-construction-works-8th-edition, accessed April 24, 2020.

Fewings, Peter. Construction Project Management: An Integrated Approach, Second Edition. London: Routledge, 2005, pp 293-301.

Hanscomb. Yardsticks for Costing: Cost Data for the Canadian Construction Industry, 2018 Metric and Imperial. Rockland, MA: Gordian, 2018.

Turner, J. Rodney, ed. Gower Handbook of Project Management, Fifth Edition. Burlington, VT: Gower, 2014.

Kirk, Stephen J. and Alphonse Dell’Isola. Life Cycle Costing for Design Professionals, Second Edition. New York, NY: McGraw-Hill, 1995.

Toronto Regional Real Estate Board. Rough/Advanced Guide to Construction Costs. Toronto: TREB Commercial Network, 2020.